Digital platforms have invested heavily in user onboarding security. Banks, fintech apps, e-wallets, marketplaces, mobility platforms, gaming services, and social applications increasingly use identity verification to confirm that a new account belongs to a real person.

But account security does not end after onboarding.

Once an account has been created, verified, and actively used, it becomes a valuable target. Instead of registering a new account with fabricated information, fraudsters can attempt to take control of an existing trusted account and abuse the privileges that the legitimate user has already established.

This is account takeover fraud.

Passwords, one-time codes, and device checks remain essential. However, they do not always prove that the person performing an action is still the rightful account holder. Face recognition can provide an additional identity verification layer when risk increases.

The goal is not to ask users to complete a selfie check every time they open an app. The goal is to apply stronger identity verification selectively, at the moments when the platform needs greater confidence.

What Is Account Takeover Fraud?

Account takeover fraud occurs when an attacker gains unauthorized control of a legitimate user account.

The attacker may obtain login credentials through phishing, credential stuffing, malware, social engineering, leaked databases, or weak password-reset processes. In other cases, the attacker may hijack an active session or manipulate an account recovery flow.

Once inside the account, the attacker may attempt to:

- Change the registered email address or phone number

- Reset the password

- Add a new trusted device

- Disable authentication factors

- Add a new payment destination

- Withdraw funds or transfer stored value

- Redeem loyalty points or virtual assets

- Access sensitive personal information

- Use the account to scam other users

The challenge is that the platform may continue to treat the attacker as a trusted user. The credentials may be correct, the session may appear valid, and the account already has an established history.

This is why digital platforms need stronger verification at high-risk moments.

Why Passwords and OTPs Are Not Always Enough

Passwords verify whether a user knows a secret. One-time passwords confirm access to a registered device or communication channel.

Both are important, but neither automatically proves that the person completing the action is the account owner.

A password may be stolen. An SMS code may be intercepted or obtained through social engineering. A user may approve a fraudulent request without understanding the consequences. A password-reset flow may become a weaker route into the account than the normal login process.

This creates a broader identity question:

Does the person attempting this action still match the trusted identity behind the account?

Face recognition helps platforms answer that question by comparing a newly captured face against a trusted reference image associated with the account.

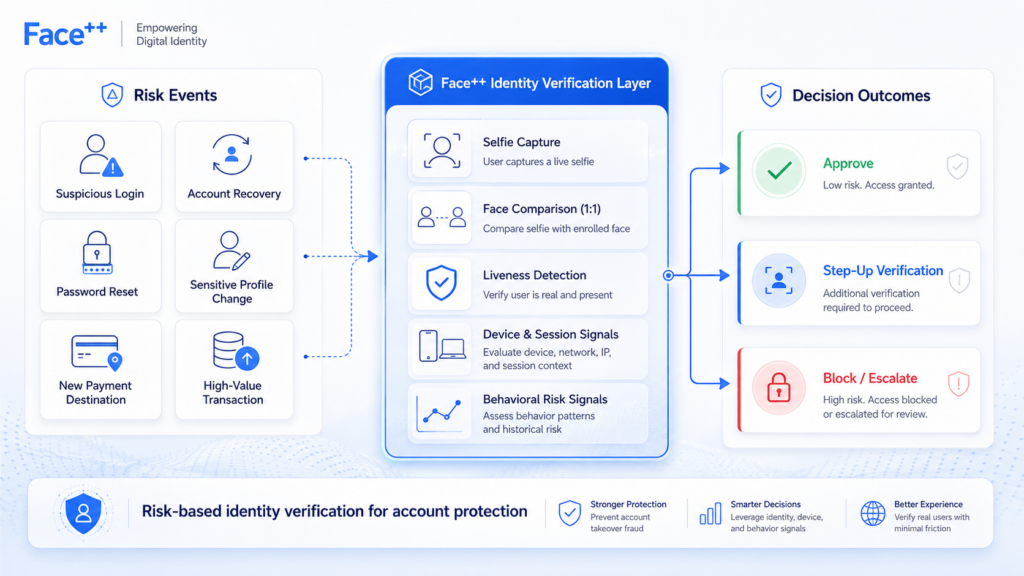

Where Face Recognition Fits in Account Protection

Face recognition should not replace passwords, passkeys, device binding, multi-factor authentication, or session security controls.

Instead, it can serve as a step-up verification layer when the platform detects unusual or higher-risk activity.

A typical 1:1 face verification flow works as follows:

- The platform identifies a risk event.

- The user completes a selfie capture or short face verification flow.

- The captured face is compared with the trusted reference image associated with the account.

- The platform evaluates the result together with liveness, device, session, and behavioral signals.

- The system approves, rejects, or escalates the action based on the overall risk level.

The trusted reference image may come from an identity document portrait collected during onboarding, a verified selfie, or another approved enrollment process.

This allows platforms to strengthen security without adding friction to every user interaction.

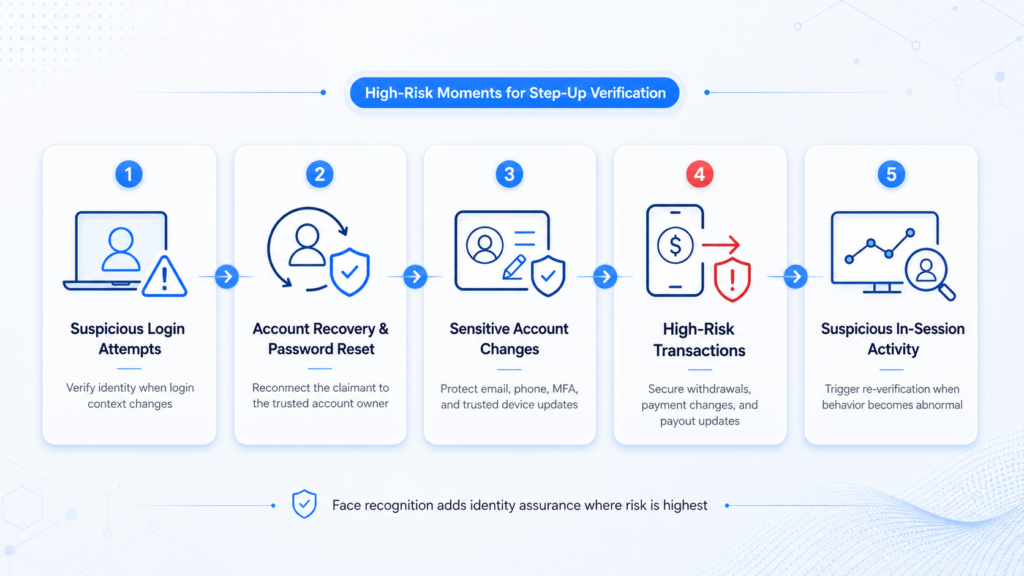

Five High-Risk Moments Where Face Recognition Adds Value

1. Suspicious Login Attempts

A login attempt becomes more suspicious when the context changes significantly, such as:

- A new or unrecognized device

- An unusual geographic location

- Repeated failed login attempts

- Abnormal IP activity

- Access shortly after a password reset

Instead of blocking every unfamiliar login, the platform can trigger face verification for selected sessions.

A successful face match provides additional confidence before access is granted or a new device is trusted. For attackers relying only on stolen credentials, the barrier becomes significantly higher.

2. Account Recovery and Password Reset

Account recovery is one of the most sensitive parts of the user journey.

A platform may have strong login security but still expose a weaker fallback process. If a fraudster can reset a password using compromised contact details or manipulated support interactions, the recovery flow becomes an easy route into the account.

Face recognition can strengthen recovery by reconnecting the claimant with the identity previously verified during enrollment.

For higher-risk recovery requests, the platform can evaluate device and network signals, request a live face capture, compare it against the trusted reference, and route suspicious cases to additional verification or manual review.

Recovery should not be treated as a shortcut around authentication. In many cases, it should be treated as a higher-risk identity event.

3. Changes to Sensitive Account Information

Fraudsters often attempt to secure long-term control of a compromised account.

They may change the email address, phone number, password, recovery settings, authentication factors, or trusted devices.

Platforms can trigger face verification before allowing users to:

- Replace a registered phone number

- Change the primary email address

- Disable multi-factor authentication

- Add a new trusted device

- Modify recovery contacts

- Update high-risk profile information

This creates an additional approval step before an attacker can lock the legitimate user out of the account.

4. High-Risk Transactions and Payment Changes

For fintech apps, e-wallets, marketplaces, and other transaction-based services, the highest business risk may occur after login.

An attacker may access the account successfully but still need to complete a sensitive action, such as:

- Adding a new payout destination

- Changing payment details

- Initiating a high-value withdrawal

- Transferring stored value

- Redeeming loyalty points

- Purchasing valuable digital goods

Face recognition can be applied as a transaction-level verification step.

The platform does not need to challenge every transaction. A small, familiar payment may proceed normally, while a large withdrawal to a newly added destination may require stronger identity verification.

This creates a risk-based experience with minimal friction for legitimate users.

5. Suspicious Activity During an Active Session

Not every account takeover begins with a suspicious login.

An attacker may hijack an active session or gain access after the user has already authenticated. Platforms therefore need to monitor what happens after login.

Potential risk signals include:

- Rapid changes to multiple account settings

- Sudden access to sensitive pages

- Abnormal transaction velocity

- A new payout destination followed by an immediate withdrawal

- Repeated attempts to modify security settings

- Behavior inconsistent with the user’s normal activity

When the session risk score increases, the platform can pause the action and request a new identity check.

This introduces continuous trust rather than one-time trust.

Face Match Alone Is Not Sufficient

Face recognition answers an important question:

Does the captured face match the trusted reference identity?

But this is not the only question that matters.

A fraudster may obtain a victim’s profile photo, social media image, or recorded video. More advanced attackers may attempt to use replay attacks or manipulated media during verification.

This is why liveness detection is an important companion layer.

Liveness detection helps determine whether the face comes from a real person participating in the current session rather than a photo, replayed video, mask, or other spoofing medium.

A stronger verification decision combines:

- Face comparison

- Liveness detection

- Device and session signals

- Behavioral risk indicators

- Transaction context

- Account history

- Risk-based thresholds

The security value comes from orchestration, not from a single model output.

From Static Login to Risk-Based Identity Verification

A mature account protection strategy should not treat every user and every action the same way.

Most legitimate users should be able to complete routine actions without unnecessary interruptions. Stronger verification should be introduced only when the risk profile justifies additional friction.

A practical decision framework may include four levels:

Low Risk: Allow

The user logs in from a familiar device and performs routine actions. The platform allows the journey to continue without additional verification.

Medium Risk: Step Up

The user logs in from a new device or attempts an unusual action. The platform triggers face verification, liveness detection, or another secondary check.

High Risk: Escalate

The session includes multiple risk signals, such as a recent password reset, a new device, and a new payout destination. The platform requests stronger verification or routes the case to manual review.

Critical Risk: Block

The platform identifies clear signs of spoofing, repeated failed attempts, or abnormal automation. The action is rejected, and the user may be notified through trusted channels.

This model helps platforms improve security without damaging the experience of legitimate users.

How Face++ Supports Account Takeover Prevention Workflows

Face++ provides face recognition APIs and SDKs that can support identity verification, secure authentication, and risk-based account protection workflows.

Face Comparing (1:1) verifies whether two faces belong to the same person. It can compare a newly captured face against a trusted reference image and return a confidence score with configurable similarity thresholds.

For digital platforms, this capability can support:

- Login verification

- New-device verification

- Account recovery checks

- Sensitive profile change approval

- Payment authentication

- Step-up verification for high-risk actions

Liveness detection can complement face comparison by checking whether the captured face is live rather than a photo, video, or mask.

In more complex fraud scenarios, Face Search (1:N) can also support broader identity analysis by identifying similar faces across a predefined collection. This can help fraud teams investigate whether suspicious identities or organized fraud patterns appear across multiple accounts.

The appropriate architecture depends on the business model.

A social platform may trigger face verification after suspicious recovery attempts. A digital wallet may apply it before a high-value withdrawal. A marketplace may use it when a seller changes payout details.

The common principle is the same:

Identity verification should not stop after onboarding.

Conclusion

Account takeover fraud exposes a fundamental limitation in static account security.

A password may be correct. An OTP may be entered. A session may appear valid.

But the platform still needs to determine whether the person performing a high-risk action is the legitimate account holder.

Face recognition helps bridge that gap.

By combining 1:1 face comparison, liveness detection, device intelligence, session monitoring, and risk-based decisioning, digital platforms can introduce stronger identity checks exactly where they matter most.

The goal is not more friction.

The goal is trusted access throughout the entire account lifecycle.

FAQ

What is account takeover fraud?

Account takeover fraud occurs when an attacker gains unauthorized control of a legitimate user account and uses it to change account details, access data, transfer funds, or perform other unauthorized actions.

How does face recognition help prevent account takeover?

Face recognition compares a newly captured face against a trusted reference associated with the account. This helps verify the account holder during suspicious logins, recovery flows, sensitive profile changes, and high-risk transactions.

Should platforms require face verification for every login?

Not necessarily. A risk-based approach is usually more effective. Familiar, low-risk activity can proceed normally, while suspicious sessions and high-risk actions trigger step-up verification.

Can face recognition replace multi-factor authentication?

No. Face recognition works best as part of a layered security architecture that includes device binding, possession-based authentication factors, session controls, and risk scoring.

Why is liveness detection important?

A face match alone cannot prove that the user is physically present. Liveness detection helps reduce spoofing risks involving photos, replayed videos, masks, or manipulated media.