Introduction

Digital onboarding has become a core infrastructure layer for fintech companies, digital banks, telecom operators, lending platforms, insurers, payment companies, and government digital identity projects across Latin America and Southeast Asia.

In Latin America and the Caribbean, the fintech ecosystem grew from 703 companies in 2017 to 3,069 in 2023, according to IDB and Finnovista research reported by Reuters. Many of these companies are focused on expanding access to financial services for unbanked or underbanked users.

In Southeast Asia, the digital economy is also scaling quickly. The 2025 e-Conomy SEA report from Google, Temasek, and Bain & Company says ASEAN’s digital economy is expected to surpass $300 billion in gross merchandise value by 2025. At the same time, ASEAN’s Digital Masterplan emphasizes that data protection, cybersecurity, and digital trust are essential for secure digital service adoption across industries.

For onboarding teams, the challenge is clear: approve legitimate users quickly while detecting fake identities, stolen documents, mule accounts, synthetic identities, deepfakes, and account abuse. This is why face recognition, eKYC, biometric verification, liveness detection, document verification, and AML/KYC workflows are now central to customer onboarding software.

Below is a practical comparison of seven face recognition and eKYC providers frequently evaluated by digital onboarding teams in LATAM and Southeast Asia. The list is not a fixed ranking. It is a vendor shortlist based on public product capabilities, regional relevance, and common onboarding use cases.

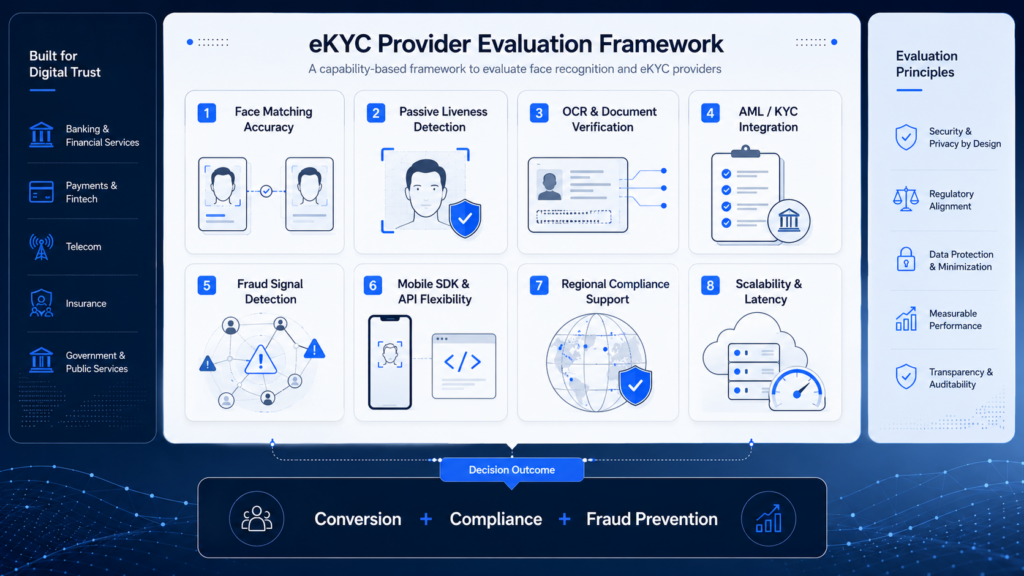

What Businesses Should Look for in a Face Recognition & eKYC Provider

A strong face recognition and eKYC provider should help businesses reduce onboarding fraud without creating unnecessary friction for real users. For LATAM and SEA markets, vendor evaluation should cover both technical performance and operational fit.

Key evaluation criteria include:

- Passive liveness detection: Can the system detect photo attacks, replay attacks, masks, deepfakes, and injection attempts without forcing users through complex gestures?

- Face matching accuracy: Can it compare a live selfie against an ID portrait reliably across lighting conditions, camera quality, age variation, and demographic diversity?

- OCR and document verification: Does it support passports, national IDs, driver’s licenses, residence permits, and country-specific identity documents?

- AML and KYC integration: Can it support sanctions screening, PEP checks, adverse media, KYB, proof of address, or ongoing monitoring?

- Mobile SDK and API flexibility: Does it support app, web, H5, API, and custom workflow integration?

- Fraud detection capability: Does it combine biometric, document, device, behavioral, and risk signals?

- Regional compliance support: Can it adapt to Brazil, Mexico, Colombia, Indonesia, Thailand, Vietnam, the Philippines, Malaysia, and other target markets?

- Scalability and latency: Can it handle high-volume onboarding during market launches or promotional campaigns?

- Multilingual onboarding: Does the user flow support local languages and region-specific UX requirements?

- Implementation complexity: Is the solution a plug-and-play workflow, a configurable platform, or a biometric API layer that requires more internal engineering?

The best provider is not always the one with the most features. It is the one that best matches the business model, fraud exposure, regulatory requirements, onboarding volume, and internal product capability.

Top 7 Face Recognition and eKYC Providers for Digital Onboarding in LATAM & SEA

Jumio

Overview

Jumio is a global identity verification provider focused on online ID verification, biometric verification, fraud prevention, and KYC/AML compliance. Its identity verification product is designed to automate online identity checks, prevent identity fraud, and simplify KYC/AML compliance during customer onboarding.

Jumio is often evaluated by digital banks, fintech platforms, crypto exchanges, payment companies, marketplaces, and other regulated digital businesses that need an enterprise-grade digital KYC provider.

Key Features

- Online identity verification

- Government ID document verification

- Selfie-to-ID biometric verification

- Liveness detection

- KYC/AML compliance support

- Fraud prevention and risk signal capabilities

- Enterprise onboarding workflows

Strengths

Jumio performs well as a mature, end-to-end identity verification solution. It is suitable for businesses that need structured onboarding, compliance controls, auditability, and fraud prevention in one platform.

For LATAM and SEA companies operating in regulated sectors, Jumio’s value is strongest when onboarding must support both user conversion and compliance review.

Potential Considerations

Jumio may be more suitable for enterprise buyers than smaller teams looking for lightweight face recognition APIs. Pricing, workflow configuration, local document coverage, and manual review requirements should be tested before deployment.

Best For

Digital banks, fintech companies, crypto exchanges, payment providers, marketplaces, lending platforms, and regulated financial services.

Sumsub

Overview

Sumsub is a full-cycle verification platform covering identity verification, business verification, AML screening, transaction monitoring, case management, and fraud prevention. Its documentation states that it supports identity documents for individuals from more than 200 countries.

For LATAM and SEA, Sumsub is relevant for businesses that need more than face recognition or ID document checks. It is commonly evaluated when onboarding must connect user verification, business verification, AML compliance, and risk operations.

Key Features

- ID document verification

- Face matching and liveness checks

- KYC and KYB workflows

- AML, sanctions, and PEP screening

- Case management and manual review tools

- Transaction monitoring and fraud prevention modules

- API and workflow configuration

Strengths

Sumsub is strong for companies that need a broad compliance and fraud prevention stack. It can support multi-market onboarding where consumer KYC, merchant onboarding, KYB, and ongoing monitoring need to operate together.

This makes it relevant for fintech, crypto, iGaming, trading, marketplace, and cross-border payment companies operating across multiple jurisdictions.

Potential Considerations

Because Sumsub covers many modules, buyers should define the scope clearly before implementation. A company looking only for face verification may not need the full platform, while a regulated financial services provider may benefit from the broader compliance workflow.

Best For

Fintech platforms, crypto exchanges, iGaming companies, trading platforms, marketplaces, payment providers, and cross-border financial services.

Veriff

Overview

Veriff provides AI-powered identity verification and KYC solutions for global digital businesses. Its official product materials state support for identity verification in more than 230 countries and territories, covering more than 12,500 ID documents.

Veriff is relevant for LATAM and SEA businesses that need automated digital onboarding, biometric verification, assisted image capture, and fraud signal analysis across mobile-first user journeys.

Key Features

- Identity and document verification

- Biometric verification

- Passive liveness detection

- Assisted image capture

- AML screening

- Device and network analytics

- Customizable end-user flows

- Multilingual onboarding support

Strengths

Veriff is strong for high-volume digital platforms that need automation, speed, and user-friendly onboarding. Its passive liveness and assisted capture capabilities are useful in markets where onboarding abandonment is a major business concern.

For consumer-facing apps in LATAM and SEA, Veriff can be suitable when the business needs fast identity verification at scale across many countries.

Potential Considerations

Buyers should validate performance using local ID documents, low-end Android devices, unstable network conditions, and real capture environments. False rejection rates, manual review workload, and local language UX should also be tested.

Best For

Fintech, crypto, gaming, mobility, marketplaces, age verification, payment platforms, and global consumer apps.

Entrust / Onfido

Overview

Onfido is now part of Entrust. Entrust completed the acquisition of Onfido in 2024, expanding its AI-powered identity verification and identity-centric security portfolio.

Entrust Identity Verification supports digital onboarding through document verification, biometric verification, identity verification SDKs, workflow orchestration, and fraud protection capabilities. Its documentation includes product guides for document and biometric verification, fraud protection, and compliance-related identity verification solutions.

Key Features

- Document verification

- Biometric verification

- Liveness and selfie verification

- Identity verification SDKs

- Workflow orchestration

- Fraud protection signals

- Enterprise identity security alignment

Strengths

Entrust / Onfido is strong for enterprise identity programs that need onboarding, authentication, and identity security under a broader vendor ecosystem. It is suitable for companies that value mature documentation, structured workflows, and enterprise implementation support.

For banks, fintechs, and payment companies, Entrust / Onfido can support regulated onboarding flows where identity verification is part of a larger trust and security architecture.

Potential Considerations

Companies that previously evaluated Onfido should review current Entrust product packaging, roadmap, support model, and commercial terms after the acquisition. Buyers should also validate regional document coverage and implementation complexity in each target market.

Best For

Banks, fintech companies, payment providers, workforce verification, enterprise identity programs, and regulated digital platforms.

ADVANCE.AI

Overview

ADVANCE.AI is a Southeast Asia-focused provider of digital identity verification, KYC/KYB, AML, compliance, and risk management solutions. Its official site describes the company as a provider of identity verification solutions covering document checks, facial recognition, risk intelligence, and fraud prevention.

For businesses operating in Southeast Asia, ADVANCE.AI is especially relevant because of its regional positioning and focus on banking, fintech, payments, retail, and e-commerce sectors.

Key Features

- eKYC and identity verification

- KYC and KYB workflows

- AML and compliance solutions

- Facial recognition

- Document verification

- Risk intelligence

- Fraud prevention tools

- Regional onboarding support for SEA markets

Strengths

ADVANCE.AI’s main strength is regional relevance in Southeast Asia. For companies operating in Indonesia, the Philippines, Thailand, Vietnam, Malaysia, or Singapore, local market understanding can be important for user experience, document handling, compliance alignment, and fraud prevention.

It is a practical option for SEA businesses that want identity verification, compliance, and risk management capabilities from a regionally focused provider.

Potential Considerations

Companies expanding beyond Asia should evaluate global coverage and LATAM support carefully. Regional strength in SEA does not automatically mean equal performance across Latin American markets.

Best For

SEA fintechs, digital banks, lending platforms, payment providers, e-commerce platforms, telecom operators, and regional financial services groups.

Facephi

Overview

Facephi is a digital identity provider focused on biometric verification, digital onboarding, fraud prevention, and compliance workflows. Its official materials highlight digital onboarding with document verification, biometric authentication, sanctions and PEP screening, behavioral fraud analytics, and LATAM compliance contexts such as Colombia and Brazil.

Facephi is particularly relevant for financial institutions and digital identity programs with exposure to Latin American markets.

Key Features

- Digital onboarding

- Document verification

- Biometric authentication

- Passive liveness

- AML checks

- PEP and sanctions screening

- Behavioral fraud analytics

- Compliance-focused identity workflows

Strengths

Facephi’s strength is its LATAM relevance and biometric identity focus. Its onboarding solution supports remote identity verification by capturing document information and a selfie with passive liveness, while also supporting AML checks, PEP list detection, and sanctions screening.

This makes Facephi a strong candidate for organizations that need digital onboarding and biometric authentication in Spanish- and Portuguese-speaking markets.

Potential Considerations

Companies operating across both LATAM and SEA should validate coverage, support, and performance in each target country. Product fit may vary depending on whether the use case is banking, telecom, fintech, insurance, or government identity.

Best For

Banks, fintech platforms, insurance companies, government identity projects, payment providers, and LATAM-focused digital onboarding programs.

Face++

Overview

Face++ is a face recognition and AI identity verification technology provider that is often considered when businesses need flexible biometric capabilities inside a customized digital onboarding architecture.

Unlike full-stack eKYC platforms that package document verification, AML screening, case management, and compliance workflows into one product, Face++ is more relevant for teams that want to integrate face recognition, face comparison, liveness detection, and biometric verification into their own onboarding systems.

Megvii’s FaceID solution covers ID card verification, biometric detection, and face comparison, with deployment scenarios across mobile apps, H5, and PC pages. FaceID documentation also references liveness verification, face comparison, attack prevention, and regional API endpoints such as Singapore and Indonesia, which is relevant for Southeast Asia deployment planning.

Key Features

- Face comparison for selfie-to-ID verification

- Face detection and face quality assessment

- Liveness detection for biometric anti-spoofing

- ID document verification capabilities

- Mobile app, H5, and web integration options

- API-based deployment for customized onboarding flows

- Attack prevention and biometric verification modules

Strengths

Face++ is suitable for businesses that need face recognition infrastructure rather than a fully packaged compliance platform. Its API-first approach can be useful for companies with internal product, engineering, or risk teams that want more control over the user journey, decision logic, and integration layer.

For fintech companies, telecom operators, e-wallets, lending platforms, gaming platforms, and mobility apps in LATAM and SEA, Face++ can support identity verification scenarios where face recognition is one signal inside a broader risk engine.

It can also support use cases beyond first-time onboarding, such as duplicate account detection, account recovery, step-up verification, and risk-based identity checks.

Potential Considerations

Face++ may require more internal implementation ownership than end-to-end eKYC platforms. Businesses should evaluate local document coverage, regulatory requirements, manual review processes, compliance operations, and integration resources before deployment.

For companies that need built-in AML screening, KYB, sanctions checks, case management, or full compliance operations out of the box, a broader eKYC platform may be more suitable.

Best For

Fintech apps, e-wallets, lending platforms, telecom onboarding, gaming platforms, mobility platforms, system integrators, and companies building customized AI identity verification workflows.

Key Digital Onboarding Challenges in LATAM & SEA

LATAM and Southeast Asia share similar digital onboarding pressures, but local execution varies by country. Many users are mobile-first. Identity document formats differ across jurisdictions. Customer acquisition costs can rise quickly when onboarding abandonment is high. Fraud risks also change rapidly as financial services, payment platforms, gaming apps, and digital wallets scale.

Common challenges include:

- Synthetic identity fraud: Fraudsters combine real and fake data to create identities that can pass basic checks.

- Deepfakes and injection attacks: AI-generated faces, replayed videos, and virtual camera attacks can target weak liveness systems.

- Mule accounts: Criminal networks may use recruited users, stolen IDs, or manipulated onboarding flows to open accounts for money movement.

- Document forgery: Edited scans, screenshots, low-quality images, and fake local IDs can increase review workload.

- Regulatory variation: KYC, AML, data protection, and financial crime rules differ across Brazil, Mexico, Colombia, Indonesia, Thailand, Vietnam, the Philippines, Malaysia, and other markets.

- Device and connectivity limitations: Low-end Android devices, poor cameras, unstable networks, and glare can reduce verification success rates.

- Friction versus conversion: More security steps may reduce fraud, but excessive friction can increase user drop-off.

The operational goal is not simply to add more checks. The goal is to build a risk-based onboarding flow that can approve low-risk users quickly, escalate suspicious cases, and block high-risk attempts before account creation.

How AI is Changing Biometric Identity Verification

AI identity verification is moving beyond simple selfie-to-ID matching. Modern systems increasingly evaluate multiple signals across the onboarding session.

Important trends include:

- Passive liveness detection: Users can prove presence without complex blink, nod, or head-turn instructions.

- Deepfake detection: AI models analyze synthetic artifacts, manipulated media, and abnormal video signals.

- Behavioral biometrics: Typing behavior, device handling, session activity, and interaction patterns can support fraud scoring.

- AI fraud scoring: Document, face, device, network, and behavioral signals can be combined into a risk-based decision.

- Reusable digital identity: Verified identity profiles may support faster onboarding across financial services, marketplaces, and public services.

- Remote onboarding automation: AI can reduce manual review workload while escalating suspicious cases to human analysts.

- Cross-border verification: Global and regional providers are improving support for multi-country onboarding, local documents, and multilingual user flows.

The most effective systems do not treat biometric verification as a single yes-or-no decision. They use face recognition as one layer inside a broader identity trust architecture.

Conclusion

Digital onboarding is now a strategic capability for LATAM and SEA businesses. It directly affects user growth, fraud losses, compliance readiness, and customer trust.

Providers such as Jumio, Sumsub, Veriff, Entrust / Onfido, ADVANCE.AI, Facephi, and Face++ represent different approaches to identity verification. Some are stronger as full-stack eKYC and compliance platforms. Others are better suited for biometric verification infrastructure, regional identity workflows, or API-first integration.

The right choice depends on target markets, customer risk, regulatory requirements, onboarding volume, engineering resources, and user experience goals. A digital bank in Brazil, an e-wallet in Indonesia, a lending platform in Mexico, a telecom operator in the Philippines, and a gaming platform in Thailand may all need eKYC, but their fraud patterns and compliance priorities will not be identical.

As AI-driven fraud becomes more sophisticated, biometric verification will continue to evolve from basic face matching into multi-layer identity intelligence. In LATAM and Southeast Asia, the strongest digital onboarding solutions will be those that verify real users quickly, detect fraud early, and maintain compliance without creating unnecessary friction.