Digital onboarding has become a critical growth channel for banks, fintech platforms, digital wallets, lending apps, and other regulated digital businesses. Customers expect to open an account, verify their identity, and start using services within minutes. At the same time, businesses must meet customer due diligence requirements, prevent identity fraud, and maintain a reliable audit trail.

This creates a common challenge: how can digital businesses keep onboarding fast and user-friendly without weakening compliance or fraud controls?

The answer is not to make every customer go through the same heavy verification process. Instead, leading organizations are adopting a risk-based CDD approach, where verification requirements are adjusted according to the customer’s risk level, transaction context, and fraud signals. This approach aligns with global AML/CFT principles that encourage institutions to identify, assess, and manage risk proportionately, rather than applying the same control level to every case. FATF also recognizes that digital identity systems can support customer due diligence when they are reliable, independent, and appropriate for the risk context.

What Is Risk-Based CDD?

Customer Due Diligence, or CDD, is the process of identifying and verifying customers, understanding the nature of the customer relationship, and assessing potential financial crime or fraud risks. In digital onboarding, CDD usually includes identity document capture, OCR extraction, document authenticity checks, face verification, liveness detection, screening, and risk assessment.

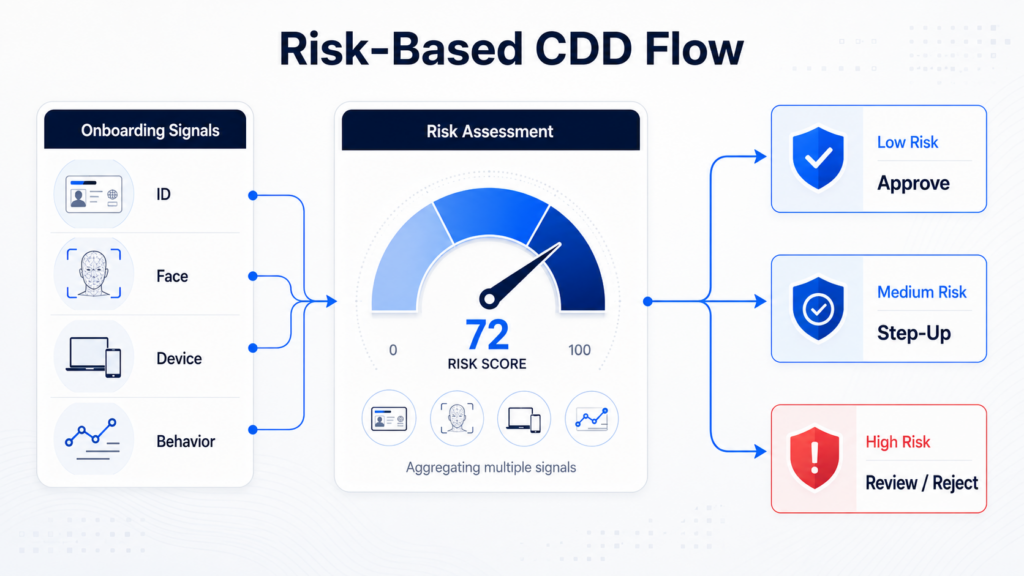

A risk-based CDD model does not treat every applicant as equally risky. Instead, it evaluates multiple signals during onboarding and determines the appropriate level of verification.

For example, a low-risk customer using a valid government-issued ID, passing face verification, showing normal device behavior, and registering from a consistent location may be approved with minimal friction. A higher-risk user, such as someone using a suspicious device, submitting a manipulated document, or showing mismatched identity data, may be routed to step-up verification or manual review.

This model helps businesses avoid two common extremes: weak onboarding controls that expose the platform to fraud, and overly strict verification flows that create unnecessary drop-offs among legitimate users.

Why One-Size-Fits-All CDD Hurts Digital Onboarding

Traditional compliance workflows were often designed for branch-based or document-heavy processes. When these workflows are directly moved online, they can create excessive friction. Every user may be required to submit multiple documents, complete repeated verification steps, or wait for manual review before accessing services.

This may improve control in some cases, but it also increases abandonment. In competitive digital markets, customers may simply move to another provider if onboarding feels slow or confusing.

At the same time, reducing verification too much creates another problem. Fraudsters actively exploit weak onboarding flows using stolen IDs, fake documents, synthetic identities, deepfakes, replay attacks, and device farms. Once bad actors enter the platform, they may create mule accounts, abuse promotions, launder funds, or take over legitimate accounts.

Risk-based CDD is designed to solve this tension. It applies stronger controls where risk is higher, while keeping the experience streamlined for trusted users.

Key Signals in a Risk-Based Digital Onboarding Flow

A strong risk-based CDD framework should combine identity, document, biometric, device, and behavioral signals. No single signal is enough. The value comes from connecting these signals into a unified risk view.

1. Identity document signals

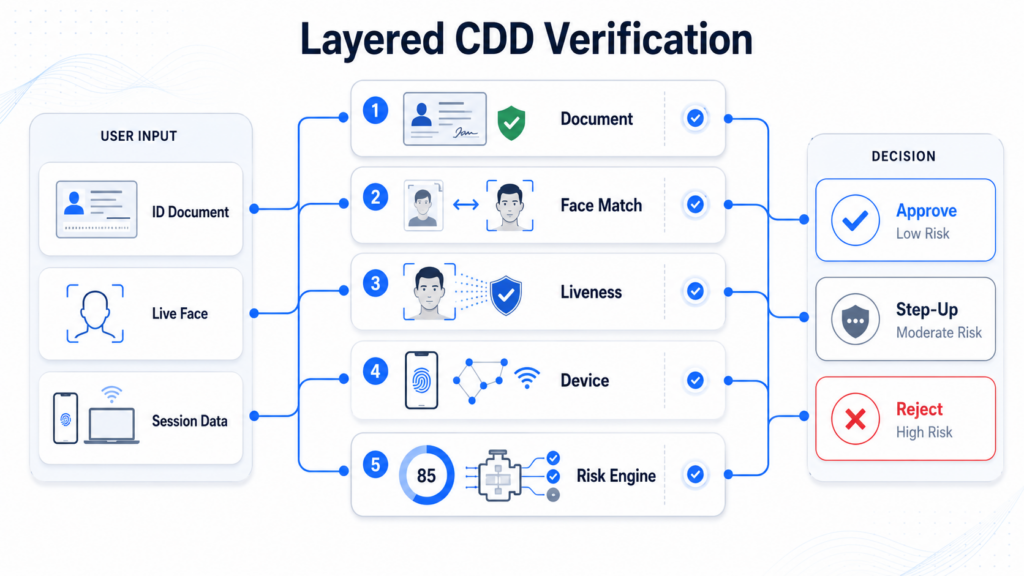

The onboarding flow starts with document capture. OCR extracts key fields such as name, date of birth, ID number, expiry date, and issuing country. Document verification then checks whether the document appears authentic, valid, and consistent.

This layer can detect issues such as expired IDs, mismatched dates, tampered portraits, abnormal fonts, copied templates, screen recapture, and image manipulation. Cross-field validation can also compare OCR fields, MRZ data, barcode data, and visual zones to identify inconsistencies.

2. Face verification signals

Face matching compares the live user’s selfie or video frame with the portrait on the identity document. This helps confirm that the person submitting the document is the legitimate document holder.

For digital onboarding, face verification is especially important because document ownership cannot be confirmed by document upload alone. A stolen or borrowed ID may look valid, but the user behind the session may not match the document owner.

3. Liveness detection signals

Liveness detection helps determine whether the user is physically present during verification. It protects against presentation attacks such as printed photos, screen replay, masks, and other spoofing attempts.

As deepfake and injection attacks become more sophisticated, liveness should not be treated as a simple camera check. A more robust approach combines face quality analysis, motion or interaction signals, environment signals, and injection attack detection to identify suspicious verification attempts.

4. Device and session signals

Fraud often appears at the device or session layer before it becomes visible in identity data. A suspicious onboarding session may involve VPN or proxy use, emulator activity, device fingerprint reuse, abnormal IP geolocation, inconsistent time zone settings, or repeated account creation from the same device cluster.

Device intelligence helps detect organized fraud patterns, especially when fraudsters attempt to create multiple accounts using different identities but shared infrastructure.

5. Behavioral and historical signals

Behavioral signals include typing patterns, interaction speed, form completion behavior, retries, failed attempts, and unusual navigation paths. These signals can be combined with historical platform data, such as previous applications, linked accounts, repeated document use, or recurring face similarity across accounts.

When these signals are connected, businesses can move from single-user verification to network-level fraud detection.

How Risk-Based CDD Improves Conversion

Risk-based CDD does not mean lowering compliance standards. It means applying the right level of control to the right user at the right time.

For low-risk users, the system can minimize unnecessary steps. The user submits an ID, completes face verification, passes liveness detection, and receives a fast approval. This improves onboarding speed and reduces abandonment.

For medium-risk users, the system can trigger step-up verification. This may include asking for an additional selfie, re-capturing the document, verifying another document type, or routing the case to manual review.

For high-risk users, the platform can block the application, flag the account, or escalate the case for investigation. High-risk triggers may include document tampering, face mismatch, failed liveness, emulator use, repeated device patterns, or identity links to previously rejected accounts.

This tiered structure allows businesses to protect conversion while maintaining strong risk controls. Legitimate users are not punished with unnecessary friction, while suspicious users face stronger verification barriers.

Building an Effective Risk-Based CDD Workflow

A practical digital onboarding workflow can be structured around four stages.

The first stage is signal collection. The system captures the identity document, face image or video, device information, session metadata, and user-submitted data.

The second stage is identity verification. OCR, document checks, face comparison, and liveness detection verify whether the user’s identity evidence is complete, authentic, and consistent.

The third stage is risk scoring. The platform combines identity signals, document signals, biometric signals, device signals, and behavioral signals into a risk score. This score should be configurable based on the company’s compliance policy, market, customer segment, and risk appetite.

The fourth stage is decisioning. Based on the risk score, the system can approve, step up, manually review, reject, or monitor the user after onboarding.

This workflow should also include audit logs. Regulators and internal compliance teams need to understand why a user was approved, rejected, or escalated. A clear audit trail helps demonstrate that the business follows a consistent and explainable CDD process. Basel Committee guidance has long emphasized the importance of sound customer due diligence standards and risk management in banking, which remains relevant as onboarding moves into digital channels.

The Role of Face++ in Risk-Based Digital Onboarding

Face++ supports digital businesses in building layered identity verification workflows for risk-based onboarding. By combining ID document OCR, document verification, face comparison, liveness detection, and identity risk signals, businesses can create a more adaptive CDD process.

Instead of relying on manual review for every user, platforms can automate low-risk approvals, identify suspicious cases earlier, and reserve human review capacity for complex or high-risk applications. This helps improve operational efficiency while strengthening fraud prevention.

For businesses operating across multiple markets, a risk-based approach is also more scalable. Different countries, document types, user segments, and regulatory environments may require different onboarding rules. A flexible verification architecture allows teams to adjust policies without rebuilding the entire onboarding flow.

Conclusion

Digital onboarding should not force businesses to choose between compliance, security, and conversion. With risk-based CDD, these goals can work together.

The key is to move beyond static identity checks and build an adaptive verification workflow. Low-risk users should experience fast and seamless onboarding. Medium-risk users should receive targeted step-up checks. High-risk users should be blocked or escalated before they can harm the platform.

As identity fraud becomes more automated and sophisticated, digital businesses need a CDD framework that is both secure and flexible. By combining document verification, face verification, liveness detection, device intelligence, and risk-based decisioning, organizations can create a digital onboarding process that supports growth while maintaining trust and compliance.