In digital onboarding, identity fraud does not always appear as a completely fake document or an obviously manipulated selfie. In many cases, fraudsters use real document images, borrowed identities, edited utility bills, or screenshots from different sources to pass basic Know Your Customer (KYC) checks.

One common risk signal is inconsistency across name and address fields. A customer may submit an identity document, proof of address, bank statement, or additional supporting file where the name, address, or date information does not fully match. These mismatches can indicate simple user error, but they can also point to synthetic identity fraud, document tampering, account mule activity, or attempted onboarding with someone else’s credentials.

For digital businesses, name and address consistency checks help turn fragmented document data into a stronger risk signal. By combining OCR, document verification, field normalization, and cross-document comparison, businesses can detect suspicious inconsistencies earlier in the onboarding process.

Why Name and Address Consistency Matters in KYC

Many regulated industries need to verify both identity and residential information. This is especially important for financial services, digital lending, payments, wallets, crypto platforms, insurance, mobility platforms, and marketplaces.

A typical onboarding flow may require users to submit:

- A government-issued ID document

- A proof of address document

- A bank statement or utility bill

- A tax document or business registration document

- A selfie or liveness check

Each document may contain overlapping identity fields. The user’s full name may appear on an ID card, bank statement, and proof of address. The address may appear on a utility bill, bank statement, or residential certificate. When these fields conflict, the platform needs a structured way to determine whether the difference is acceptable, suspicious, or high-risk.

Without automated consistency checks, many businesses rely on manual review. This increases operational cost, slows down conversion, and creates inconsistent decision-making across review teams.

Common Types of Name Mismatches

Name mismatches are not always straightforward. In many markets, names may contain multiple components, abbreviations, initials, transliterations, or different ordering rules. A strict character-by-character comparison may create false rejections, while a loose comparison may allow fraud to pass.

Common name mismatch scenarios include:

Different name order

For example, a name may appear as “Li Wei” on one document and “Wei Li” on another. Depending on the country or document type, this may be normal.

Missing middle name or initials

A bank statement may show “John A. Smith,” while an ID document shows “John Andrew Smith.” This may be acceptable if the core name components match.

Abbreviated or shortened names

Some documents use shortened given names, initials, or truncated names due to space limits.

Spelling variation

OCR errors, transliteration differences, or local spelling conventions can create minor differences.

Completely different holder name

If the ID document belongs to one person and the proof of address belongs to another, this may indicate borrowed documents, mule activity, or account takeover attempts.

The goal is not simply to label every mismatch as fraud. A strong KYC system should classify mismatch severity and route cases accordingly.

Common Types of Address Mismatches

Address comparison is often more complex than name comparison. Addresses can be written in different formats, languages, or levels of detail. Some documents may include apartment numbers, postal codes, districts, or province names, while others only show partial address information.

Common address mismatch scenarios include:

Format variation

“Apartment 5B, 12 King Street” and “12 King St., Apt. 5B” may refer to the same address.

Partial address match

One document may include the full address, while another only shows city and district.

Outdated address

A user may have recently moved, causing a mismatch between their ID document and utility bill.

Different region or country

A submitted proof of address may show a location that does not align with the declared country, phone number, IP region, or document issuer.

Edited address field

Fraudsters may alter only the address line while leaving the rest of the document unchanged. This can be harder to detect without document authenticity checks.

Effective address consistency checks need to normalize address fields before comparison. This includes removing punctuation, standardizing abbreviations, identifying address components, and comparing structured elements such as city, province, postal code, and street.

How Automated Consistency Checks Work

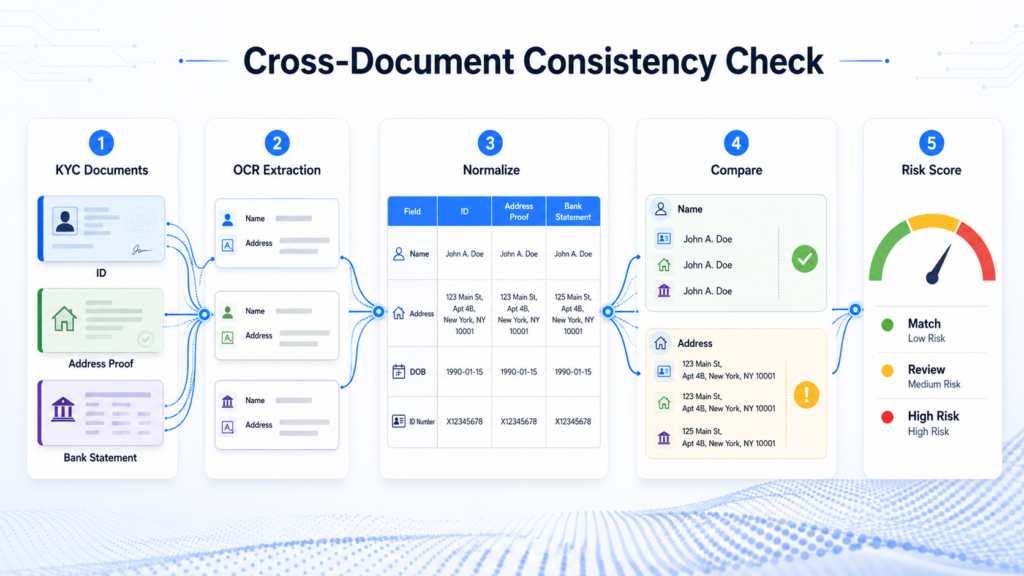

A modern KYC workflow can detect name and address inconsistencies through several layers.

1. OCR Field Extraction

The process starts with OCR. The system extracts key fields from submitted documents, including name, address, date of birth, ID number, issue date, expiry date, and document type.

For consistency checks, OCR quality is critical. If the extracted fields are inaccurate, the comparison result will also be unreliable. This is why OCR should be designed for identity documents and supporting documents, not just generic text recognition.

2. Field Normalization

Before comparing fields, the system standardizes the extracted text. For names, this may include case normalization, punctuation removal, whitespace cleanup, and component-based parsing.

For addresses, normalization may include expanding abbreviations, standardizing local address terms, removing duplicate spaces, and separating address components into structured fields.

For example, “St.” and “Street” should be treated as equivalent in many contexts. Similarly, apartment numbers and building names may need to be compared separately from the main street address.

3. Cross-Document Matching

Once fields are extracted and normalized, the system compares data across documents.

Examples include:

- ID name vs. proof of address name

- ID address vs. utility bill address

- Declared address vs. document address

- Bank statement name vs. ID name

- Document country vs. user-declared country

- Address region vs. phone number or IP region

The result should not be a simple pass or fail. A better approach is to generate a match score and risk category.

4. Document Authenticity Checks

Field consistency alone is not enough. Fraudsters may manipulate one field to create a match. For example, they may edit the name on a utility bill to match the ID document.

Document authenticity checks help identify whether the document has been altered, recaptured, screenshotted, spliced, or digitally edited. When a name or address field appears inconsistent with the surrounding document texture, layout, font, or image quality, the system can flag the document for review.

5. Risk-Based Decisioning

Not every mismatch should lead to rejection. A small formatting difference may be low risk, while a completely different name or country-level address mismatch may require manual review or rejection.

A risk-based KYC engine can classify cases into different outcomes:

- Low risk: approve automatically

- Medium risk: request additional proof

- High risk: route to manual review

- Critical risk: reject or block the application

This helps businesses balance fraud prevention, compliance, and onboarding conversion.

Red Flags to Watch For

Name and address consistency checks are especially useful when combined with other risk signals. Businesses should pay attention to patterns such as:

- The name on the ID does not match the proof of address

- The address belongs to a different country or region

- The address field shows signs of editing

- Multiple users submit documents with the same address

- The same proof of address is reused across different accounts

- OCR fields conflict with MRZ, barcode, or visual document data

- The user’s IP, phone region, and document country do not align

When multiple signals appear together, the case should be treated as higher risk.

Business Benefits of Automated Consistency Checks

Automated name and address consistency checks help digital businesses improve both security and operational efficiency.

First, they reduce manual review workload by identifying clear matches and obvious mismatches automatically. Second, they improve fraud detection by surfacing subtle inconsistencies that human reviewers may miss. Third, they create a more standardized review process, reducing subjective decision-making. Finally, they improve user experience by allowing low-risk applicants to pass quickly while only routing suspicious cases to additional verification.

For high-volume onboarding scenarios, this can significantly improve both conversion and risk control.

Building a Stronger KYC Workflow

Name and address consistency checks should not operate as a standalone rule. They work best as part of a layered identity verification workflow that includes OCR, document verification, face matching, liveness detection, device risk analysis, and risk-based decisioning.

By connecting document data across the onboarding journey, businesses can move beyond checking whether a single document looks valid. They can verify whether the user’s identity information is coherent, trustworthy, and consistent across multiple evidence points.

As digital fraud becomes more sophisticated, this cross-document intelligence is becoming a core capability for modern KYC. For businesses operating in financial services, fintech, mobility, and digital platforms, automated consistency checks can help detect mismatched KYC documents earlier, reduce fraud exposure, and support a safer onboarding experience.